In the last two days we have witnessed an incredible, rapid, steep, and perhaps unstoppable collapse in the value of the ruble. As of 9:15 AM Eastern today, the ruble is down more than 13%. By the time I publish this, that figure will be out of date. One look at today’s graph shows that there are no indicators that the ruble is even close to recovering today, or perhaps any time soon:

Notice I’ve highlighted an area in red. Late yesterday, at the height of the ruble’s devaluation, the Russian Central Bank made an emergency announcement that it was hiking interest rates from 10.5% to 17%. A massive increase like that will have a significant impact on any currency, but the move did not even erase a single day’s damage. At the start of Monday the ruble was valued at 58.12 to one dollar, and while at one point it was trading at 66.59 to the dollar, right after the rate cut was announced the value of the ruble only increased to 60.12 to the dollar, a full 2 rubles worse than the start of the day.

And as you can see, those gains were quickly erased today. Since last week the Central Bank also increased interest rates and it accomplished nothing, and since banking managers are already telling Vedomosti that “raising the interest rate to 17% is the end of the banking system,” it’s not clear that there is anything the Russian government can do to stop the ruble’s cataclysmic fall.

What is the primary reason Russia’s currency is in free fall? In order to reach this answer we have to keep in mind a basic concept — factors keeping the Russian economy from recovering may not be the same factors as what caused it to become ill. The broken hip didn’t cause the fall down the stairs, but it’s going to make it impossible to get back up.

For the moment, we’ll look at the longer-term trends, not the last two days of rapid decline.

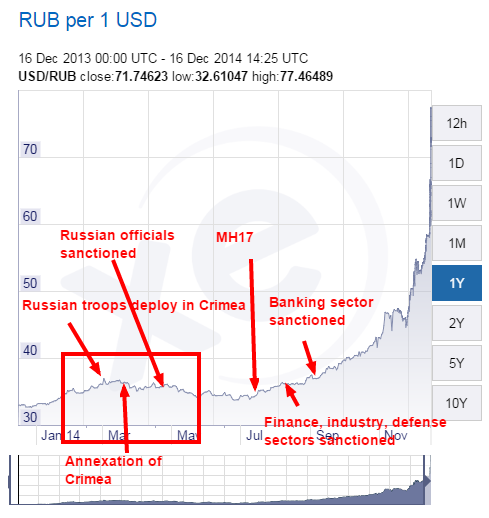

Most news analysts point to two factors driving the ruble’s collapse: drop in oil prices, and Western sanctions. The problem with this analysis is that there is very little empirical evidence to support the theory that Western sanctions are driving the ruble downward. No significant sanctions were passed during the periods of time when the ruble collapsed. In fact, immediately after nearly every set of sanctions passed in the spring and summer of 2014 Russia’s economy reacted by rallying. The chart below shows the value of the ruble against the dollar over time, with major rounds of sanctions marked (up indicates loss of value for the ruble).

As we see, Western sanctions passed from March to May had absolutely no impact on the Russian currency (Russia’s stocks hit a 9 month high at the start of July), nor did the large round of sanctions passed at the end of July (note, the ruble stayed flat after this round, the MICEX index first rallied then stayed flat for a week). Clearly, the ruble has been getting worse since July (remember that a Russian anti-aircraft weapon shot down a civilian airliner on July 17th), but it’s not clear that there is a correspondence between Western sanctions and significant drops in the ruble, or Russia’s stock indices. A better argument is that Western sanctions were corresponding with news that was shaking investor confidence.

We see significant correspondence between the fall of the price of oil and the fall of the ruble. Bloomberg charts this for us:

#Russia Ruble is going to meet Crude: Ruble down >1% as Oil prices collapse. pic.twitter.com/PrgdWjstey

— Holger Zschaepitz (@Schuldensuehner) December 10, 2014

Clearly the drop in oil prices is a major problem, and perhaps the largest problem. It’s the death knell for the Russian economy. However, once again, there are some problems with any analysis that says that oil alone is Russia’s problem. In late 2013 and early 2014, when oil was rising, it had little impact on the ruble. The ruble’s decline also starts earlier than the decline in oil. Also, yesterday, as oil stayed flat, the Russian economy fell the furthest. As the end of this chart clearly shows, it may be impossible for the Russian economy to recover unless oil rallies. To go back to our earlier analogy, oil is Russia’s broken hip (and probably the pneumonia that’s settling in) but it was not the only reason the ruble has fallen.

The problem: Putinism

At the end of 2013 many economists warned that Russia’s economy was facing stagnation — or worse. Writers for this magazine predicted that some of Russia’s policies would catch up with him in 2014 or 2015, and the Russian economy would decline. The Russian government and a certain branch of the Western media branded such predictions as Russophobia, but the reality is that the indicators were there. Oil was rallying, the Russian economy was not, and many economists pointed to Putin’s policies as the reason.

The key policies scaring off investors at the end of last year had to do with Putin’s cronyism and outdated economic policies. Putin’s Russia is not a true capitalism since large amounts of Russia’s wealth is controlled by small numbers of people with close ties to the Russian government. No example of this is more clear than the 2014 Sochi Winter Olympics, the most expensive — and corrupt — Olympic Games in the history of the world. In Sochi, Putin’s friends, family, and business partners were the main beneficiaries of a historical level of graft — with no real attempt to hide it, either. On the other hand, companies which run afoul of the Putin administration are not-infrequently prosecuted by the Putin administration for fraud and corruption. As we’ll see, this played a key role in this most recent collapse.

Putin has also been pursuing a reckless game of economic protectionism. Putin’s pet project and alternative to the European Union, the Eurasian Customs Union, has failed to attract most former-Soviet states. In response to a group of Russia’s neighbors making plans to sign EU association agreements (including, of course, Ukraine), Putin spent much of 2013 waging trade wars: banning certain imports, closing borders, passing new tariffs… as it turns out, while Putin was using these tactics to bully countries into joining the Customs Union, investors don’t like trade wars.

Despite booming energy prices, Russia’s economy was looking at the strong possibility of a recession at the start of 2014. This should have been a time where Russia’s economy was on the rise, thus creating a hedge against future bad news.

Then Russia invaded Ukraine and annexed Crimea, moves which gave Russia control of territory which is not self-sufficient and cost money to take over in the first place. And then, yes, there were sanctions. But it turns out that investors like real wars even less than trade wars. Even before sanctions, or the drop in oil prices, Russia’s stock indices and the value of the ruble were starting to decline. By the time oil started to drop, the writing was already on the wall. But as long as oil is this low, or dropping, there is virtually no chance for the Putin administration to turn things around. This is one reason why the Russian economy is falling faster than the price of oil — even if oil stabilizes, which it may not, Putin’s policies have done their damage.

Ruble crashed after Putin nationalized oil company

The Russian economy has been in decline for much of the year, but the tumble downward is much more recent. A closer look at what actually happened right when the ruble began to fall is a good indication of how Putin’s policies are an important and often ignored reason why the ruble is tumbling.

The ruble hit its first record low on September 28th, 2014, but investors weren’t talking about sinking oil prices as the main culprit at the time. In June the Russian government froze the assets of a division of the Sistema holding company, specifically the division which had acquired the Bashneft oil giant. On September 16th, before the price of oil began to plummet, Russian billionaire Vladimir Yevtushenkov was placed under house arrest. Yevtushenkov, the head of the investment company AFK Sistema, was charged with money laundering. In October, the Bashneft division was nationalized by the Russian government.

Investors panicked. Some speculated that the move was indeed related to the falling price of oil. Perhaps the Russian government was seeking more direct control over the oil market, or perhaps the government was trying to bolster the value of the ruble in advance of the fall of oil. Whatever Putin was thinking, the move did not work. Instead, investors panicked, the MICEX tumbled, and so did the ruble. While Russian stock markets did rally in October on news that the Russian government was not going to expand their investigation or seizure of Sistema, the ruble has never recovered.

The point here is that Russian investors who are paying closer attention than the media did not begin to panic because of a drop in oil prices. However, those investors who did panic see no reason to stop, and the rest of the world tuning in to Russia’s markets sees no signs of recovery any time soon.

Putin’s policies are also at least partially to blame for the reason that, in the last two days, the price of oil has gone up while the Russian economy has fallen apart. Russia’s opposition, and many Western analysts, believe that what was driving this sudden collapse are actions taken by the Russian state-owned oil company Rosneft, run by key Putin ally Igor Sechin. Yesterday Rosneft issued a series of bonds with a lower yield than Russian government bonds. It appears that Russian state-owned banks then used these bonds as collateral to borrow foreign currency, effectively swapping rubles for foreign currencies (I say appears because it’s unclear — Bloomberg calls the deal “opaque“). Bloomberg’s analysis — blame Putin’s dictatorship:

Central Bank technocrats have been worried that the government would force them to print rubles for the direct funding of industries, primarily the military industrial complex and the state companies run by Putin friends. The Central Bank’s obvious complicity in the Rosneft deal means the pressure is on, and the Central Bank is caving. It cannot prevent the funds loaned to corporations in special deals such as Rosneft’s from destabilizing the currency and fueling market panic. Besides, the Rosneft deal sends a clear signal to market players that some of them are more equal than the others. That is a sure way to foster distrust and send the ruble into a speculative tailspin regardless of what happens to the oil price.

All who try to understand Russia’s stormy markets today should keep in mind that they are dealing with a dictatorship, whose monetary authorities can only conduct reasonable policy until Putin says otherwise.

But what did the Russian government do after the ruble started to fall? Once again, Putin’s own policies have failed to stabilize the currency. One reason for this — stubbornness and lack of transparency. Last year, while economists were predicting a recession, the Kremlin downplayed this threat. Recently, the Russian government has taken small steps to address the falling ruble, but has not admitted that there is a serious problem until the last 48 hours. Even then, Russian media continues to downplay the extent of the crisis.

Since each step has not been enough, investors shrugged off these fixes. But each failed fix makes it harder to stop the decline of the ruble. Last week, when Russia’s Central Bank only raised interest rates by 1%, the ruble fell further because investors were expecting a larger hike. Bloomberg borrows a phrase from Bill Clinton here to show that nothing the Russian government has done has stabilized the ruble:

It’s Oil, Stupid: Putin powerless to stop the ruble’s slide. http://t.co/fEjtsOVXXk pic.twitter.com/US5PhIsxkx

— Bloomberg VisualData (@BBGVisualData) December 14, 2014

That analysis is now old. Obviously, the big news now is that the Central Bank’s emergency option, a 6.5% rate hike, also did not fix the problem (it seems to have helped a bit, though). The latest news is that as of an hour and a half ago foreign-exchange brokers has suspended trading of the ruble because of the volatility of the markets. That may actually stabilize the price of the ruble for a while, but it’s hard to call that a fix.

In summary, Putin’s policies left the Russian economy unprepared for the day energy prices declined, his policies spooked investors at the worst possible time, and his policies have failed to stop the bleeding.

What’s next?

This question is a bit hard to answer because Russia’s “opaque” realities. As Financial Times points out, Russia has massive foreign currency reserves, but most experts expect those are running out quickly:

With foreign reserves falling & the rate hike not having the desired effect, is the next step capital controls? (6/6) pic.twitter.com/tv5auFVIbi

— Ferdinando Giugliano (@FerdiGiugliano) December 16, 2014

The massive interest rate hike how not significantly increased the value of the ruble, but it will have a significant impact on anyone with a mortgage, car payment, or other debts in Russia. It’s only a matter of time, then, that inflation will have a substantial impact on the ground in Russia. Trading Economics reports that inflation was already having a noticeable impact on the price of food:

Year-on-year, the highest upward pressure came from food and non-alcoholic items (+12.5 percent), with sugar posting the highest increase (+20.8 percent), followed by cereals and vegetables (+20.5 percent) and meat and poultry (+18.2 percent). Housing, water, electricity and gas prices grew at a faster 8 percent, mostly driven by a rise in water cost (+13.9 percent) and an increase in rent prices (+13.1 percent). Cost of transports advanced 6 percent and clothing and footwear grew 5.5 percent.

On a monthly basis, consumer prices accelerated to 1.3 percent, for the third consecutive month, mainly boosted by a surge in cost of food and non-alcoholic beverages (+2.4 percent).

If interest rates don’t control the ruble, then people will have higher mortgages and higher food prices — it won’t matter that their savings accounts will be generating more money if they can’t afford to put any money there.

Now foreign companies may stop doing business in Russia out of fear that they’ll have no idea how to price goods. This news just in:

BREAKING: Apple halts Russia online sales due to “extreme fluctuations” in the ruble. http://t.co/4pcbZO5iGo pic.twitter.com/E8mFdipbd2

— CNBC Now (@CNBCnow) December 16, 2014

“Doomed” is the word many analysts and journalists have been throwing around today. With no way out, what will Putin do next? In February, having suffered a significant defeat in Ukraine with the ouster of ally Viktor Yanukovych, Putin responded by annexing Crimea and invading the Donbass. If Putin is out of options to fix his economy, he may just have to change the narrative once again.